Dollar Extends Slide on More Dovish Fed Remarks

- Fed’s Bostic and Kashkari join the ‘no more hikes needed’ camp

- PPIs and Fed minutes on tap ahead of tomorrow’s CPIs

- Aussie and kiwi helped by China stimulus reports

- Wall Street rebounds as Fed hike probability falls

Fed dovish chorus grows louder

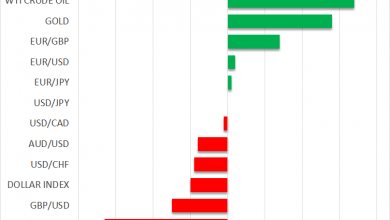

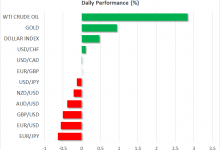

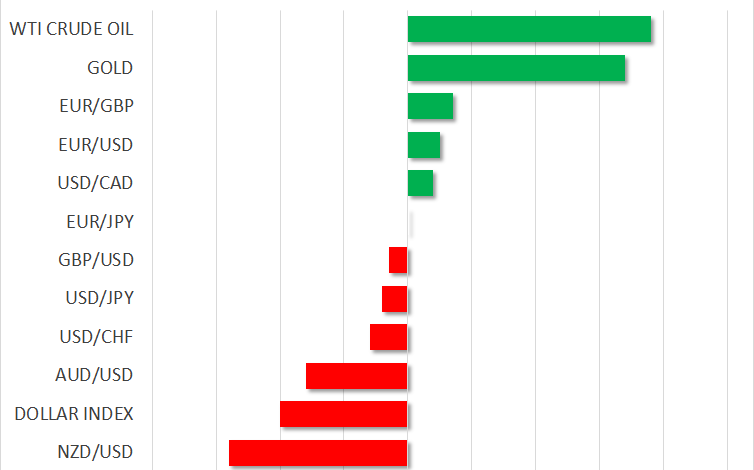

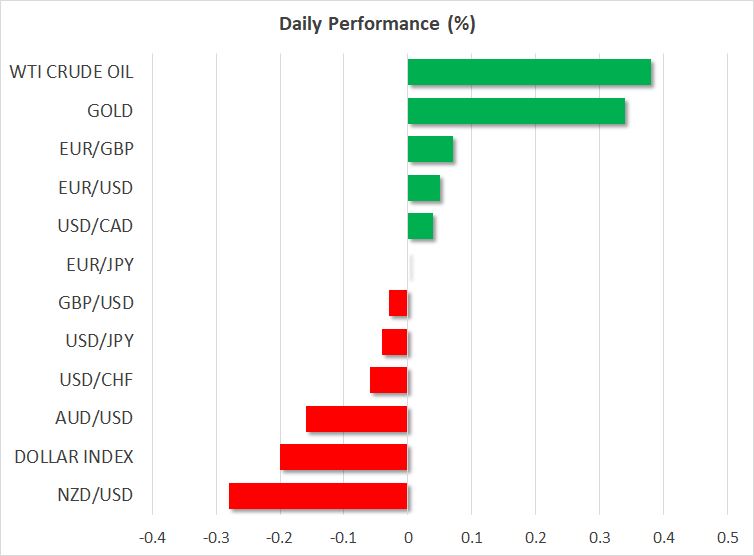

The US dollar continued drifting lower against most of the other major currencies on Tuesday, as several Fed officials appeared in their dovish suits this week, signaling that they may not need to tighten as much as initially thought. The only currency failing to post gains against the greenback was the Japanese yen.

Following remarks on Monday by Fed Vice Chair Philip Jefferson and Dallas Fed President Lorie Logan that the tightening in financial conditions due to the surge in Treasury yields might negate the need for additional hikes, Atlanta Fed President Rafael Bostic and Minneapolis Fed President Neel Kashkari expressed similar views yesterday.

That said, Kashkari, who has been an outspoken hawk during this hiking cycle, added that if higher long-term yields are higher due to expectations about what the Fed might do, then they may need to satisfy those expectations in order to maintain yields at those levels.

The slide in both the dollar and yields following the latest Fed rhetoric suggests that indeed the market may be mainly driven by such expectations, and thus, calling with certainty the end of this hiking crusade and a trend reversal in the dollar may be premature.

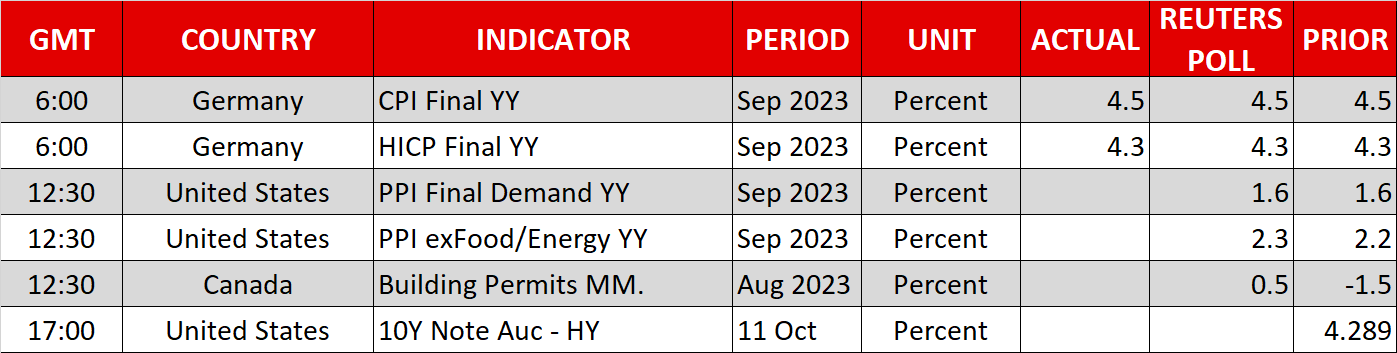

PPIs to set the stage for CPIs, Fed minutes also on tap

Currently, investors are assigning around a 30% probability for another rate hike by December, but that could well change if upcoming data suggests that inflation is stickier than previously thought. Traders may be sitting on the edge of their seats in anticipation of tomorrow’s CPI numbers for September and will get an early glimpse of where inflation may be headed as the PPIs for the month are due today.

The headline rate is forecast to have held steady at 1.6% y/y, while the core one is anticipated to have ticked up to 2.3% y/y from 2.2%. That said, conditional upon the core PPI accelerating, the risks surrounding the headline rate may be tilted to the upside as oil prices have been in a steep uptrend during most of September. An upside surprise may raise speculation that Wednesday’s CPI rates could also come in higher than expected and thereby allow the dollar to recover some of its recently lost ground.

The minutes of the latest FOMC gathering are also on today’s schedule but given that the market has already heard updated views by several policymakers this week, any reaction may be limited. Investors may pay more attention to a speech by Fed Governor Christopher Waller. Waller spoke yesterday, highlighting the central bank’s determination to bring inflation down to 2%, but he did not comment on upcoming monetary policy moves. It will be interesting to see whether he does today.

China hopes allow aussie and kiwi to add gains

The currencies that took the most advantage of the dollar’s slide were the risk-linked aussie and kiwi, which may have been helped by a report saying that China is considering new stimulus measures to shore up its wounded economy. With recent data suggesting that the world’s second-largest economy may have begun bottoming out, aussie and kiwi traders may now turn their attention to China’s inflation and trade numbers, due out on Friday.

Should the data corroborate the view that the Chinese economy is stabilizing, both currencies may extend their recoveries. However, with China’s property sector still suffering, those recoveries may just be treated as decent upside corrections rather than the beginning of healthy long-lasting uptrends.

Wall Street cheers prospect of no more rate hikes

Wall Street closed in the green on Tuesday as equity investors cheered the prospect of no more hikes by the Fed. The gains also suggest that investors may have turned their focus away from the conflict in the Middle East between Israel and Palestine, despite Israel retaliating against Hamas with missile attacks in Gaza.

Although they may keep an eye on the conflict due to concerns of further escalation, market participants will likely pay more attention to the upcoming inflation data for now. Anything pointing to hotter-than-expected inflation could prompt some selling as the probability of another rate increase by the Fed could increase again.