Yields Slide as Fed Tones Down Hawkish Talk, Stocks Shrug Off Middle East Flareup

- Higher yields prompt a rethink at the Fed as policymakers turn cautious

- But less hawkish tone pushes yields lower, boosting equities

- Ongoing tensions in Middle East further pressure yields, keep gold supported

- Oil slips slightly while dollar braces for more Fed speak, CPI data

Fed has second thoughts about additional tightening

As markets wait anxiously to see how far the latest conflict between Israel and Hamas will escalate, Fed policymakers provided some soothing words to jittery investors already caught wrong footed by the recent surge in yields.

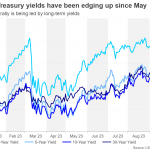

The relentless rise in long-term borrowing costs since the summer expanded the rout in bond markets to equity markets, stifling risk appetite. But with the next FOMC decision only three weeks away, the Fed is taking stock of financial conditions amid the lack of clear signals from the economic data.

The first clue to a possible turnabout in policy came to light last Thursday when San Francisco Fed President Mary Daly suggested that financial markets have “done the work” for the Fed as the 10-year Treasury yield has risen by about 40 basis points since the September meeting. Speaking on Monday, both Fed Vice Chair Philip Jefferson and Dallas Fed chief Lorie Logan also implied that the recent tightening in financial conditions amounts to an additional rate hike by the Fed.

Whilst that assessment would no longer hold true if Treasury yields were to reverse sharply lower, what is becoming more certain is that the Fed is inclined to wait at least until December before deliberating on the need for one final rate hike.

For the markets, the not-so-hawkish comments on the back of Friday’s super-strong jobs report couldn’t have come at a better time as stocks have been tarnished in recent weeks from the repeated ‘higher for longer’ message. And although the violence in the Middle East is seen as having only a limited fallout for now, it has nevertheless added a new layer of uncertainty to the outlook, so the shift in tone from the Fed is much welcome from a risk sentiment perspective.

Stocks cheer drop in bond yields

The 10-year Treasury yield dipped from Friday’s close of 4.78% to a low of 4.62% on Tuesday as trading resumed for US Treasuries. European government bond yields have also retreated from last week’s decade highs, pulling regional stock indices sharply higher today. In Asia, the major markets closed in positive territory, with the exception of Chinese indices, which were weighed by a warning from property giant Country Garden that it may default on its international debts.

On Wall Street, shares rebounded for a second straight session and futures point to further gains today. It seems that the conflict in Israel and Gaza has been a boon for energy and defence stocks, whose gains have more than offset losses for airlines, which have been hit by the disruption to air travel in the region.

Oil and gold off highs but stay supported

As for oil prices, WTI and Brent crude futures are paring their losses from earlier in Tuesday’s session, indicating ongoing upside momentum despite the initial panic from the weekend headlines having faded. Gold is also holding on to most of its gains, finding support in the $1,850/oz region after earlier spiking to $1,865/oz.

The very modest pullbacks in crude oil and gold suggest there is still some unease regarding the volatile situation in the Middle East. Whether demand holds up for the two commodities will probably depend on what Israel decides to do next, specifically if they will launch a ground invasion of the Gaza Strip.

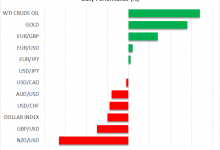

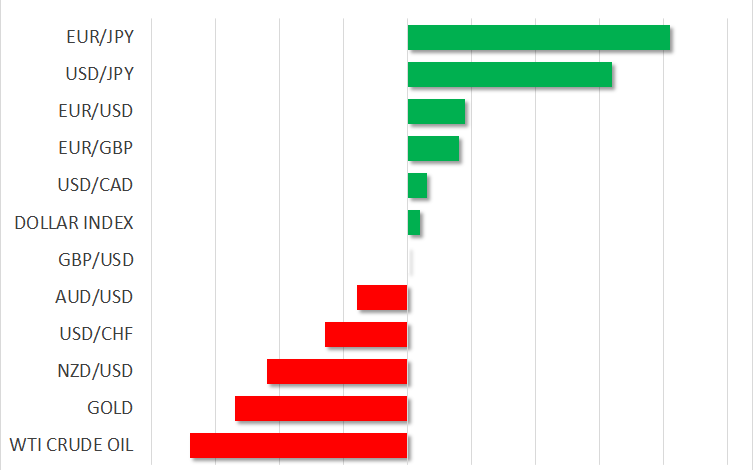

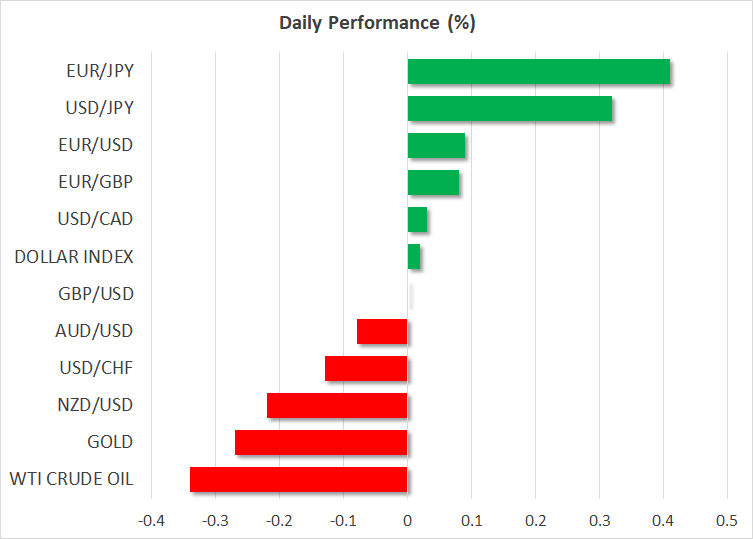

Safe havens dollar and yen ease

In the meantime, the mood was somewhat lighter in FX markets as the safe havens US dollar and Japanese yen were both softer on Tuesday. The euro edged up above $1.06 even as ECB policymakers signalled that rates have likely peaked, while sterling clawed above $1.2250 ahead of monthly UK GDP readings on Thursday. The aussie was flat today after an impressive rebound yesterday.

With more Fed speakers lined up to speak this week, including Waller and Kashkari today, and the September CPI report due on Thursday, the upbeat mood will undergo several tests.