Mighty dollar turns to US inflation data and Fed minutes

- Dollar stabilizes ahead of FOMC minutes and US inflation report

- Inflation expected to cool further – is the Fed done raising rates?

- Minutes due at 18:00 GMT Wednesday, inflation 12:30 GMT Thursday

Dollar sizzles

The US economy continues to display impressive resilience. Economic growth accelerated over the summer and is projected to have reached an annualized 4.9% in the third quarter according to the Atlanta Fed GDPNow model, as consumers continue to spend and the labor market remains in great shape.

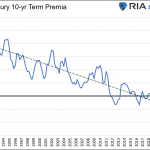

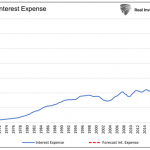

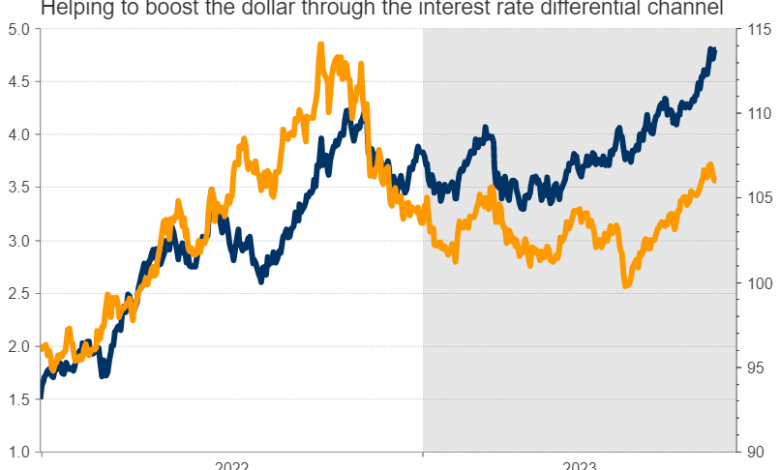

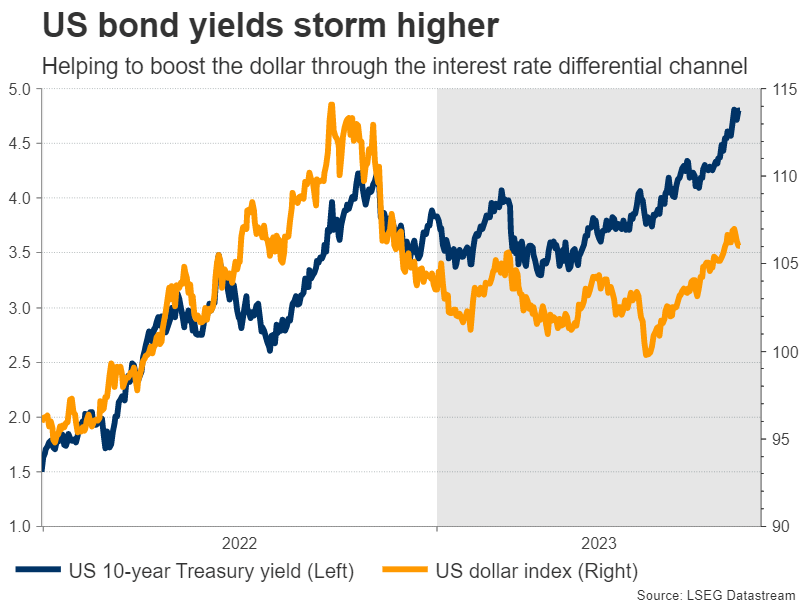

With the economy not slowing down, the Fed has adopted the view that interest rates will need to remain higher for a longer period of time to defeat inflation. This notion coupled with a sharp increase in debt issuance to fund budget deficits has pushed US bond yields to their highest levels since the financial crisis, turbocharging the US dollar.

Interest rate differentials have essentially widened in the dollar’s benefit, as US yields have risen much more aggressively than foreign ones. And with the Treasury set to continue flooding the markets with newly-issued bonds this quarter, this upside pressure will likely persist for some time.

Beyond all this, the dollar has also benefited from the worsening outlook for other currencies. The euro has been haunted by recession concerns, the British pound is grappling with a weaker labor market and fragile risk sentiment in the markets, while the yen has been devastated by the Bank of Japan’s refusal to raise interest rates.

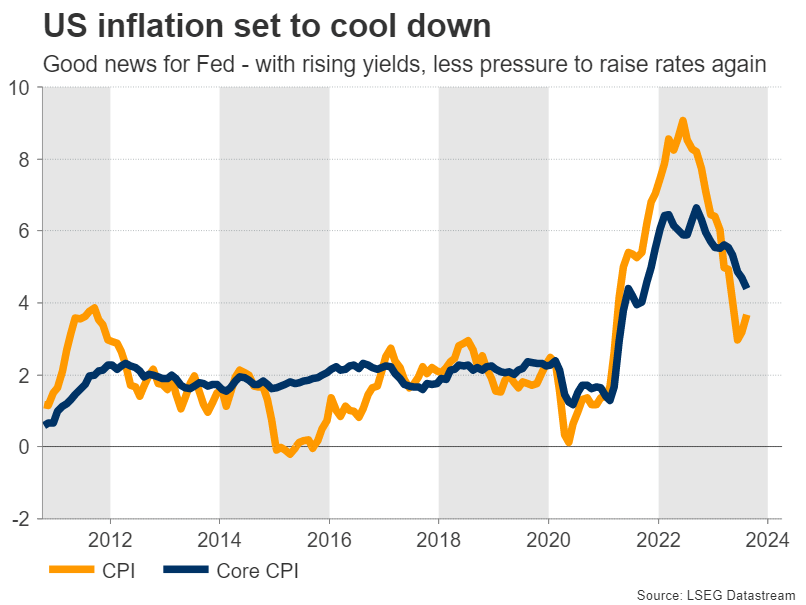

Inflation set to cool

Turning to the upcoming releases, inflation as measured by the CPI is anticipated to have lost steam on a yearly basis. The headline CPI rate is seen at 3.6% in September from 3.7% previously, while the core rate that excludes food and energy prices is expected to have declined to 4.1% from 4.3% previously.

Ahead of this dataset, the Fed will release the minutes of its September meeting, where the Committee refrained from raising interest rates but revised its implied rate path higher, fueling the ‘higher for longer’ narrative. Investors will dissect the minutes for more insights into this discussion.

The two main questions are whether the Fed will raise rates one final time this year and how long interest rates will remain at such high levels. Markets are still pricing in a 35% probability for the Fed to hike rates again by December.

However, that is highly unlikely, as the bond market has already done the heavy lifting for the Fed. The recent spike in long-dated US yields has the same effect as raising interest rates several times, so monetary policy has already been tightened lately. As such, there’s less pressure on the Fed to act again.

Dollar outlook and key levels

All told, the US dollar offers the ‘full package’ at this stage – the highest real rates among the major economies, the strongest economic growth, and safe haven qualities thanks to its reserve currency status. The US economy has been shielded by the government’s massive deficit spending, which has simultaneously safeguarded growth and pushed yields higher.

In contrast, there’s little to suggest the slowdown in Europe or China is approaching its conclusion. Leading indicators continue to paint a gloomy picture for both economies and stimulus measures have been scarce. Hence, the theme of American exceptionalism remains intact for now.

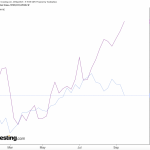

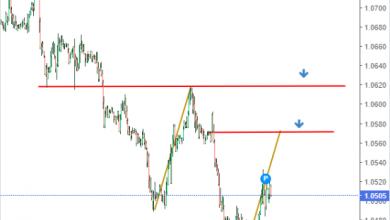

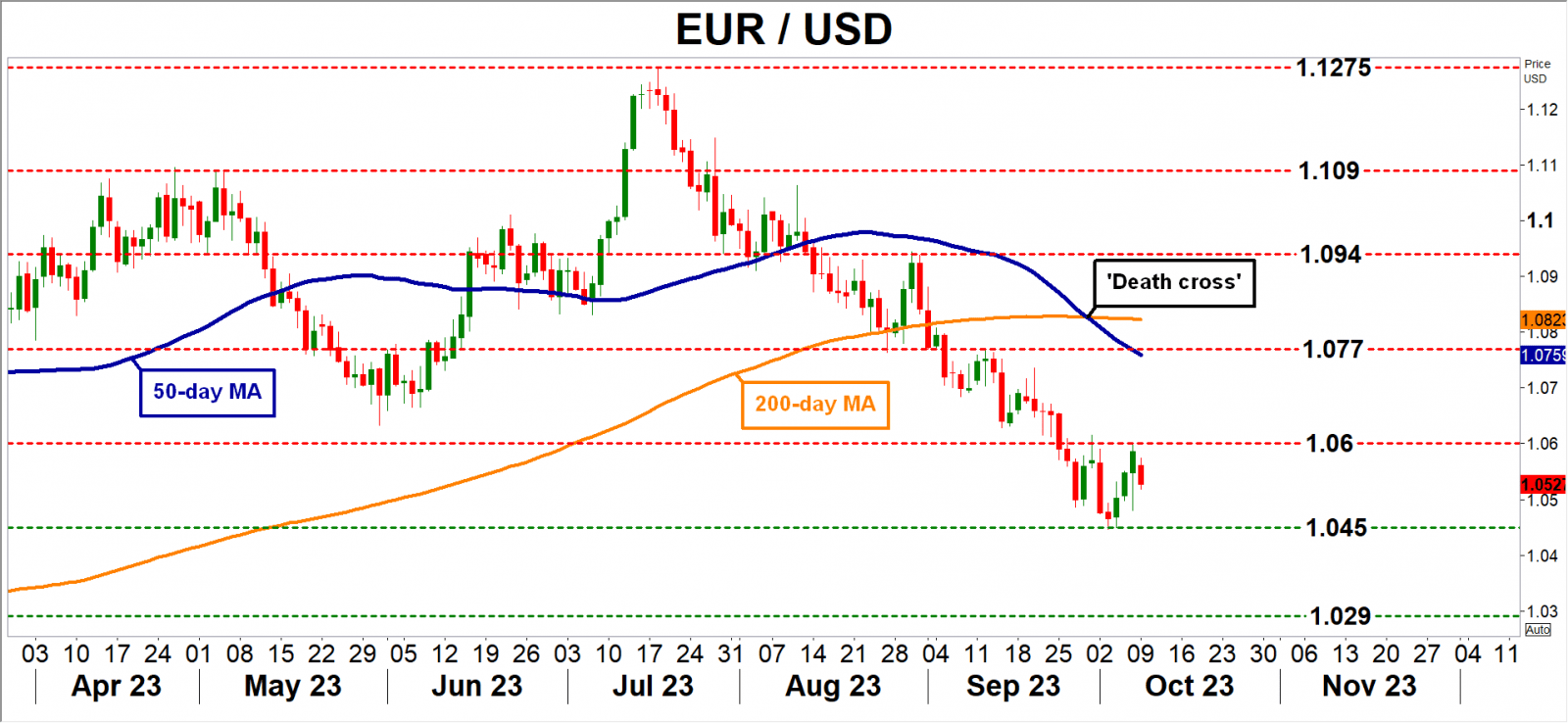

The charts tell the same story as a ‘death cross’ has formed in euro/dollar, with the 50-day moving average crossing below the 200-day one. That’s usually a negative sign. The most important level to watch on the downside is the recent low near 1.0450, while on the upside, any advances could stall around the 1.0600 region.