Are Strong 2023 Gains a New Bull or Just a Bear-Market Rally in Disguise?

Yesterday I reviewed numbers that show that the 2023 advance in the S&P 500 Index continues to post a high return when set against historical calendar-year results. Encouraging, but it’s still premature to dismiss the view that the market remains in a bear-market rally.

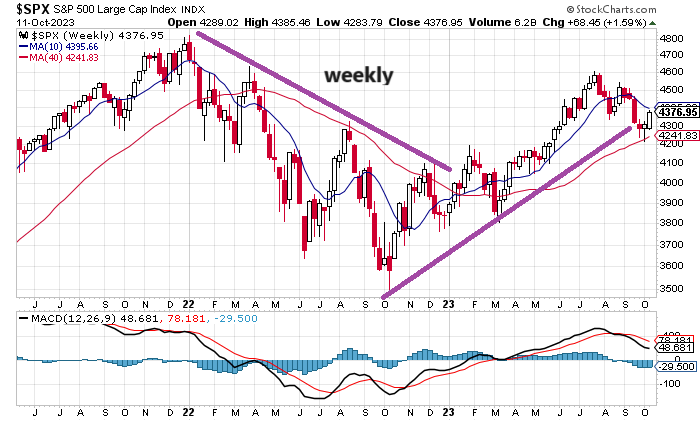

Let’s start with the current trend profile for the S&P 500. As the chart below reminds us, the market has enjoyed a strong bounce off of the previous low of a year ago. The rebound has stumbled lately and is testing the upside trend, inspiring fresh doubt about what happens next.

SPX-Weekly Chart

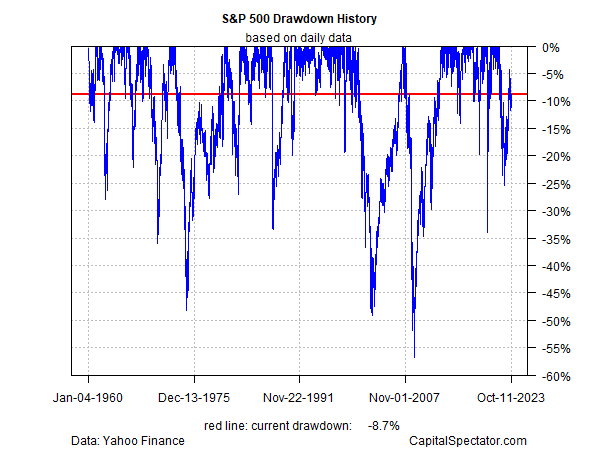

Despite the 14.0% year-to-date gain through Oct. 11, the S&P 500 has yet to fully recover from its steep loss in 2022. This is clear when we look at the S&P 500 through a drawdown lens. The current 8.7% peak-to-trough decline suggests that bear-market conditions still apply until the previous peak in January 2022 is regained and the market moves decisively above that point.

S&P 500-Drawdown History

S&P 500-Drawdown History

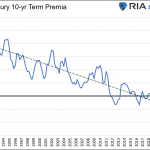

The recent rise in Treasury yields is a factor for expecting that stocks will face headwinds in the near term. The current yield for the 10-year Note is 4.58% (Oct. 11), which is close to a 16-year high. The long-term expected return for stocks is arguably higher, but the gap has surely closed by more than a trivial degree in recent weeks.

As investors weigh the risk-free return in government bonds against the higher but far more volatile and uncertain ex-ante performance in equities, the case has strengthened for trimming equity allocations.

The counterpoint favoring stocks is that the economy still looks set to post a faster pace of growth in the upcoming third-quarter GDP report while corporate earnings are on track to rebound.

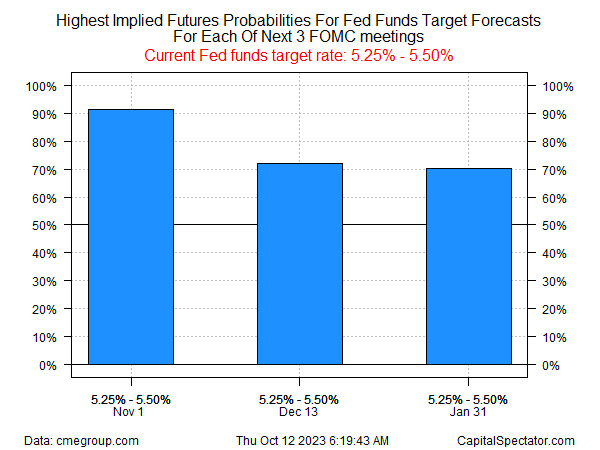

Meanwhile, there’s fresh support for thinking that the end of the rate hikes by the Federal Reserve has arrived. Fed funds futures, for instance, are pricing in a path over the next several meetings that leaves the current 5.25%-to-5.50% target rate unchanged.

Fed Fund Futures Data

Fed Fund Futures Data

Offsetting the optimism is the Israel-Hamas conflict, along with the continuing uncertainty linked to the war in Ukraine.

There are always risks, of course, and the stock market generally tends to climb a wall of worry eventually. Will that historical precedent continue? Yes, in time. But in the near term, it’s hard to imagine that a sustainable rally that takes out the previous 2022 high is imminent.

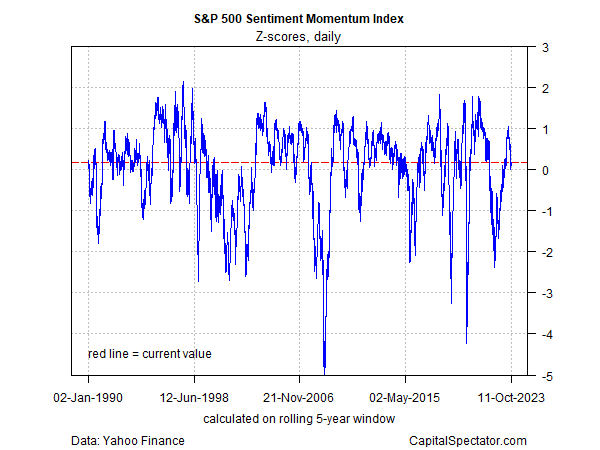

One reason for adopting a relatively neutral stance on the equity risk outlook: trend activity looks middling at the moment, based on CapitalSpectator.com’s Sentiment Momentum Index.

The tailwind that fired up stocks a year ago was based on an extremely oversold condition. With that catalyst long gone, investors are left to consider the key question: What catalysts will ignite a fire that drives the market above its previous high?

S&P 500-Sentiment Momentum Index

S&P 500-Sentiment Momentum Index

For the moment, the possibilities don’t translate into a compelling forecast that an upside breakout is about to start.