Despite rout, bond strategists stay tethered to falling yield forecasts

FILE PHOTO: An eagle tops the U.S. Federal Reserve building’s facade in Washington, July 31, 2013. REUTERS/Jonathan Ernst/File Photo

By Sarupya Ganguly

BENGALURU (Reuters) – Bond market strategists are holding on to their forecasts for U.S. Treasury yields to decline by year-end, as well as a view that 10-year yields have peaked, despite being proven wrong within days of each of the previous two monthly Reuters polls.

The latest predictions come despite a strong U.S. economy, widespread expectations the Federal Reserve will keep interest rates high well into next year, and a bleak fiscal outlook with substantial amounts of debt coming to market.

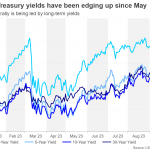

Yields on longer maturities had risen around a full percentage point from lows in July, with a major sell-off in recent weeks pushing 30-year T-bond yields to a recent peak of 5.05%, and 4.89% for 10-year notes – the highest since 2007.

Bond prices move inversely to yields.

The 10-year note yield — which has fallen to 4.56% following a flight to quality after Palestinian Islamist group Hamas launched a massive attack on Israel last weekend — was expected to decline roughly 30 basis points (bps) to 4.25% by year-end.

Most of the 55 respondents in the Oct. 6-11 poll, the bulk of them sell-side firms, continued to forecast lower yields by end-year, albeit modestly higher than thought in last month’s poll.

Goldman Sachs expects the U.S. economy to falter, calling for a fourth quarter “growth pothole”, which helps explain their forecasts for about a 25 bps fall in 10-year yields from current levels by year-end, roughly similar to the poll median.

Much depends on the Fed, which appears determined to leave the federal funds rate in its 5.25-5.50% range for an extended period following a tightening campaign that began in March 2022. Inflation is still running above target and the economy is close to full employment.

Some big banks, like Societe Generale (OTC:SCGLY), have made substantial changes to their yield forecasts, putting off an expected cooling in the world’s biggest economy.

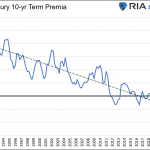

“Markets are preoccupied with finding the fair value for bond yields, conscious of a likely rebuilding of term premia at the long end of curves,” SocGen market strategists wrote in their latest client note, raising their end-year 10-year yield forecast by 75 bps to 4.50%.

“In the near term, bond yields are likely to retest recent highs. The tightening of financial conditions from higher rates should cause economic weakness over the medium-term.”

But a near three-quarters majority, 19 of 26, who answered an extra question on whether the 10-year yield had already peaked said it had, a roughly similar proportion as in the last two Reuters polls.

Asked what will be the major driver of bond yields over the remainder of the year apart from Fed policy and the economy, about 65% of respondents, 12 of 19, cited either the fiscal outlook or the near-term supply of Treasuries due to hit the market.

The U.S. Treasury has already issued a record supply of debt this year to finance large deficits – and more is yet to come.

“The bulk of the issuance has been in shorter paper and bills, and that’s being absorbed very easily by money market funds and just people parking cash. The real issue is around who the buyers of longer paper will be,” said Craig Brothers, co-head of fixed income at Bel Air Investment Advisors.

“Longer-end buyers are trying to extract a bigger premium because of the amount of supply that’s been issued and the amount of future supply that will be issued.”