Rising Borrowing Costs Strain Households in the UK and US

© Shutterstock

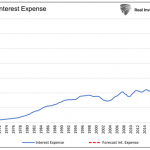

Tuesday’s Financial Policy Summary from the Bank of England has warned of impending financial hardships as households grapple with increased borrowing costs. The warning comes amidst 14 consecutive interest rate hikes that have pushed the current rate to 5.25%.

Households are allocating more of their income towards clearing debts such as credit card bills, a trend that is expected to continue. Despite consumer debt still being below its 2007 peak, high-interest rates have led to a significant increase in long-term mortgages (30 years or more) from 4% to 12% within just two years. Consequently, there has been a modest rise in arrears, although still low historically.

The report also reveals that the poorest individuals, predominantly renters who represent the majority of the UK population as per Sky News analysis, are increasingly depending on credit cards for daily expenses. Despite these economic challenges and potential worse-than-expected conditions, the UK banking system stands prepared to support households and businesses and is resilient to geopolitical risks.

Simultaneously, a survey by the Federal Reserve Bank of New York, polling 1,300 households weekly, reveals growing concern among Americans about missing debt payments. The perceived risk has risen to 12.5%, particularly among those under 40 with some college education and households earning less than $50,000 annually.

Inflation and higher interest rates are impacting lower-income individuals and those with lower credit scores most significantly. The resumption of student loan repayments is adding further stress. Borrowing is seen as more challenging than last year, with expectations of tighter future credit conditions.

For the first time in 2023, credit card debt has exceeded $1 trillion, and the average credit card APR is now at 24.45%. Despite these challenges, household spending growth remains stable at 5.3%. However, expected short and medium-term inflation growth and a 3.7% rise in consumer goods prices may exacerbate the situation.

Credit card delinquency rates have increased but were kept artificially low due to stimulus payments and reduced spending during the pandemic. More people plan to use ‘Buy Now Pay Later’ plans for holiday shopping, indicating a shift in payment methods. While there’s an expectation of continued inflation growth, long-term inflation is expected to stabilize. The September inflation number is set for release on Wednesday.