Marketmind: Oil soothes but jobs dictate

FILE PHOTO: A pump is seen at a gas station in Manhattan, New York City, U.S., August 11, 2022. REUTERS/Andrew Kelly/File Photo

A look at the day ahead in U.S. and global markets from Mike Dolan

The bond blast upending world markets has been partly smothered by sharply falling oil prices for now – but September’s U.S. employment report will dictate direction from here.

Oil prices scrabbled for a toehold Friday but were on course for their worst week since March as demand fears driven by rising interest rates and restive stock markets were compounded by another partial lifting of Russia’s fuel export ban.

U.S. crude oil has recoiled almost 9% this week and prices have lost almost 14% peak-to-trough since last Thursday’s high above $95 per barrel. The year-on-year oil price is now falling again and tracking losses of 5%.

That’s a significant relief for the inflation part of the bond blowup and will help keep a lid on U.S. pump prices.

But to the extent the oil price is flagging renewed concerns about global growth – in part due to the relentless rise in borrowing rates – can be seen in a retreat in commodity prices in general. Copper prices fell to their lowest of the year on Thursday and core commodity indexes are back at August levels.

Two-year U.S. inflation expectations in the bond market have plunged about 30 basis points to just 2.13% over the past two weeks – as near as makes no difference to the Federal Reserve’s target.

Whether that darkening demand picture holds or not will again hinge on the critical U.S. employment report out later on Friday – where a marginal slowing of monthly payroll growth to 170,000 last month is expected, alongside a downtick in the jobless rate to 3.7%.

This week’s surprisingly soft private sector payrolls data from ADP was countered by other readings showing still modest weekly jobless claims, relatively contained layoffs in September and a rebound in job openings in August.

All to play for then.

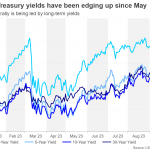

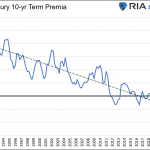

And the latest Fed soundings indicate that the screaming rise in Treasury yields to new 16-year highs close to 5% – a jump of at least half a percentage point in 10-year rates – may have achieved the sort of additional credit tightening that obviates the need for another Fed policy rate hike.

San Francisco Fed boss Mary Daly said that with monetary policy “well into” restrictive territory and Treasury yields so high, the central bank may not need to raise rates further.

All of which sees U.S. bond yields retain an uneasy calm into the jobs numbers. Ten-year yields hovered about 4.75% on Friday – still off Tuesday’s peak at 4.88%.

Implied rates from Fed futures markets pulled back the chances of another hike in the cycle to less than 50%.

Seeing some potential light at the end of the tunnel, Wall St stocks staged a late comeback close to opening levels on Thursday and stock futures were steady ahead of today’s open.

The dollar stayed on the backfoot for now too.

The other side of the bond market angst – U.S. fiscal policy stasis and the prospects of a government shutdown again next month – remained unresolved as Republicans moved to appoint a new House speaker after their unprecedented ouster of Kevin McCarthy from the post this week.

Former President and leading candidate for next year’s White House race Donald Trump said he’s endorsing Congressman Jim Jordan for the post – an appointment that won’t encourage any bets on congressional compromises to avert a shutdown.

And that mixed picture of fiscal dysfunction and a potential economic hiatus from furloughing thousands of government workers is the backdrop to Treasury secretary Janet Yellen’s trip to the annual International Monetary Fund and World Bank meetings in Morocco next week.

Elsewhere in the corporate world, shares of Tesla (NASDAQ:TSLA) fell 1.47% to $256.22 premarket after the electric vehicle giant stepped up its aggressive discounting and cut prices of its Model 3 and Model Y vehicles in the U.S. by about 2.7% to 4.2%.

In M&A news, Exxon Mobil (NYSE:XOM) is in advanced talks to acquire Pioneer Natural Resources (NYSE:PXD) in a deal that could value the Permian shale basin producer at about $60 billion, people familiar with the matter said on Thursday.

Key developments that should provide more direction to U.S. markets later on Friday:

* U.S. Sept employment report, Aug consumer credit; Canada Sept employment report

* Federal Reserve Board Governor Christopher Waller

(By Mike Dolan; Editing by Toby Chopra [email protected]. Twitter: @reutersMikeD)